Understanding Mortgage Default Insurance

January 22, 2021

Mortgage default insurance, commonly referred to as mortgage insurance, is often confused with homeowner/property insurance or mortgage/life insurance, but there are big differences. Homeowner/ property insurance protects the individual’s home and possessions in the home against damages including loss, theft, fire or other unforeseen disasters. Mortgage/life insurance is designed to repay any outstanding mortgage debt in the event of the homeowner’s death or long-term disability.

Mortgage default insurance increases the opportunities for homeownership with a low down payment, as saving for a 20 per cent down payment can be difficult in today’s housing market. There are two types of mortgage options: conventional mortgages, which are loans with a minimum 20 per cent down payment, and high-ratio mortgages, which are loans with less than 20 per cent down payment.

In Canada, mortgage insurance is required by the Government of Canada on all high-ratio mortgages. The insurance protects the mortgage lender only against a loss caused by non-payment of the mortgage by the borrower, and it is not a protection for the homeowner. However, the mortgage insurance enables borrowers to purchase a home with a minimum down payment of only five per cent.

Mortgage default insurance is provided by insurers such as Canada Mortgage and Housing Corporation (CMHC), Sagen (previously known as Genworth Canada) and Canada Guaranty. Each mortgage insurer has its own criteria for evaluating the borrower and the property, and it decides whether or not a mortgage can be insured. The lender, and not the borrower, selects the mortgage insurer. It is possible that the mortgage application can be approved by the lender, but might not be approved by the insurer.

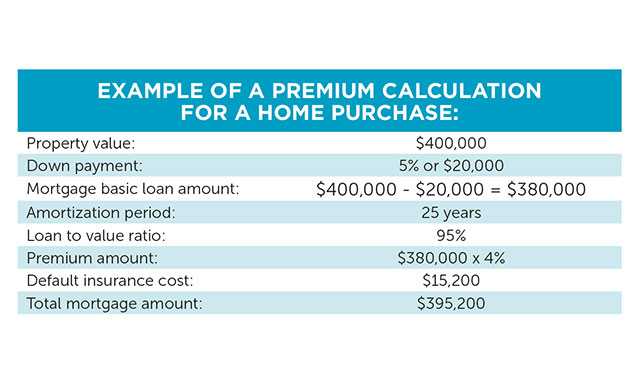

The mortgage default insurance premium is a one-time charge and it is paid by the borrower to the lender. The premium can be paid in a single lump sum at the time of closing or it can be added to the mortgage amount and repaid over the amortization period (or the life of the mortgage). The cost of default insurance is calculated by multiplying the amount of the funds that are being borrowed by the default insurance premium, which typically varies between 0.60 per cent and 5.85 per cent. Premiums vary depending on the amortization period of the mortgage, the loan to value ratio, the size of the down payment and the product.

* The cost of default insurance is subject to change if the purchase price or appraised value, the amount of down payment or the amortization changes. The final premium and the cost of the mortgage default insurance will be disclosed in the mortgage commitment document from the lender.

It is important to note that for insured mortgage loans the maximum purchase price or as-improved property value must be below $1,000,000. The borrowers can port the mortgage loan insurance from an existing home to a new home and may be able to save money by reducing or eliminating the premium on the financing of the new home.

Since there are different products available from individual lenders and are subject to lender’s guidelines, it is important to talk to a Mortgage Expert to analyze your situation, present several options and help you decide which product works best for you.